Introduction: Why Your Financials Matter

GAAP vs. Tax Basis Financial Statements are two ways to show your company’s money and performance. GAAP gives a clear, standard picture, while tax basis focuses on taxes. Knowing the difference helps business owners make smart choices, like getting loans or planning for growth.

The Dual Language of Business: GAAP vs. Tax Basis Reporting

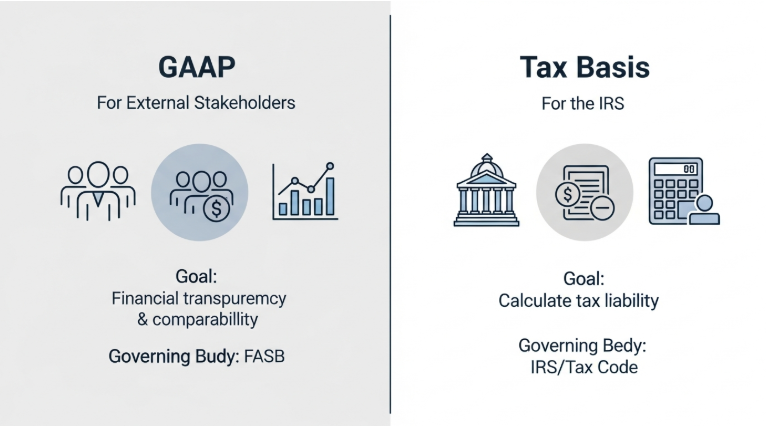

GAAP and Tax Basis accounting serve different audiences with different objectives, leading to two distinct views of a company’s financial performance.

At its core, the divergence between GAAP and tax basis reporting stems from their intended audience and objective. GAAP is designed for external stakeholders—investors, lenders, and creditors. Its goal is to provide a consistent, comparable, and transparent view of a company’s financial position. Conversely, tax basis reporting is designed for a single audience: the Internal Revenue Service (IRS). Its purpose is to accurately calculate a company’s tax liability according to federal tax code, focusing on taxable income and allowable deductions.

GAAP vs. Tax Basis Accounting: What Every Business Should Know

Most businesses use two different sets of rules to keep track of their money:

- 1. GAAP (Generally Accepted Accounting Principles): This is the “picture for your parents” (investors and banks). It uses a lot of rules to show the most honest, full picture of how healthy the business is, so people know if they should lend money or buy a part of the company.

- 2. Tax Basis Accounting: This is the “special form for the government” (like the IRS). It uses the rules from the tax law, and its main job is to figure out exactly how much tax the business needs to pay.

Where the “Report Cards” Are Different (The Important Part!)

These two report cards are different because they have different goals:

- GAAP’s goal is to show how much money the business really earned in a time period.

- How they count: GAAP makes you count money you’ve earned (like selling a toy) even if the customer hasn’t paid for it yet. And it makes you count costs (like a bill) even if you haven’t paid them yet.

- Tax’s goal is to figure out the lowest amount of tax you owe by following the law.

- How they count: Tax rules often let you count income only when you actually get the cash and count costs only when you actually pay the cash. This makes the tax number often look smaller.

These differences change three big money papers:

- The Balance Sheet: This is like the list of all your toys and all your debts. The rules change how you value big items (like machines), which makes the total number look different.

- The Income Statement: This shows how much money you made. Because they count sales and costs differently, the “profit” number is often different on each paper

- Big Decisions: If you only look at the Tax paper, the profit might look too low, and you might make a bad decision about growing the business.

Who Needs to Know About These Two Rules?

Knowing about both rules is super important for three groups of people:

- The Business Owners (The Bosses): You need to know that your company is really healthier than the lower tax number might show. You need the GAAP report to know if you are being a good business owner.

- Lenders and Investors (The Money-Givers): People who might give the business a loan or buy a part of it prefer the GAAP report. They want to see the honest, complete, and consistent picture to know their money is safe.

- Your Accounting Team (The Scorekeepers): These helpers must be good at both rules. They use the Tax rules for filing taxes, and the GAAP rules to tell the true story of the business to the bank.

Laying the Foundation: What Are GAAP and Tax Basis Financial Statements?

Before diving into the granular differences, it’s essential to establish a clear understanding of each framework’s foundation. These are not merely different formats; they are different philosophies of financial reporting.

U.S. GAAP: The Fair, Clear, and Uniform Report

- What it is: This is a big rulebook written by a group called FASB. It’s like the official rulebook for a major sports league—everyone must play by the same rules!

- Who uses it: Big, public companies (like one whose stock you can buy) must use these rules because the government (SEC) says so.

- Why they use it: Even small companies use it when they need a big loan from a bank or if they want an investor to buy a part of the company. The bank wants a fair, clear, and honest picture of the business.

- How it works (The Accrual Rule): GAAP tells the business to count money:

- When you earn it (like finishing the job), not just when the customer pays the cash.

- When you owe a bill, not just when you pay the cash.

- The Big Idea: This rule helps show the true, long-term health of the business.

Tax Basis Accounting: The Report for the Tax Man

- What it is: This set of rules is written by the government itself, in the tax law book (the IRC).

- What is its job: The main goal of this report is to figure out exactly how much tax the business has to pay the government.

- Why small companies like it: Lots of small businesses choose this way because it’s usually much simpler and often lets them count money only when they actually get it.

- Fun Fact: A business is considered “small” if it makes $31 million or less each year for the last three years.

- The Big Idea: This report is usually made to pay the smallest amount of tax possible (but still following the law!). This often makes the business look like it made less money than the GAAP report says.

Core Differences: A Detailed Look at Key Accounting Areas and Their Impact

The philosophical divide between GAAP and tax basis accounting manifests in the practical treatment of numerous financial items. These differences in timing and recognition can dramatically alter a company’s reported financial performance and position.

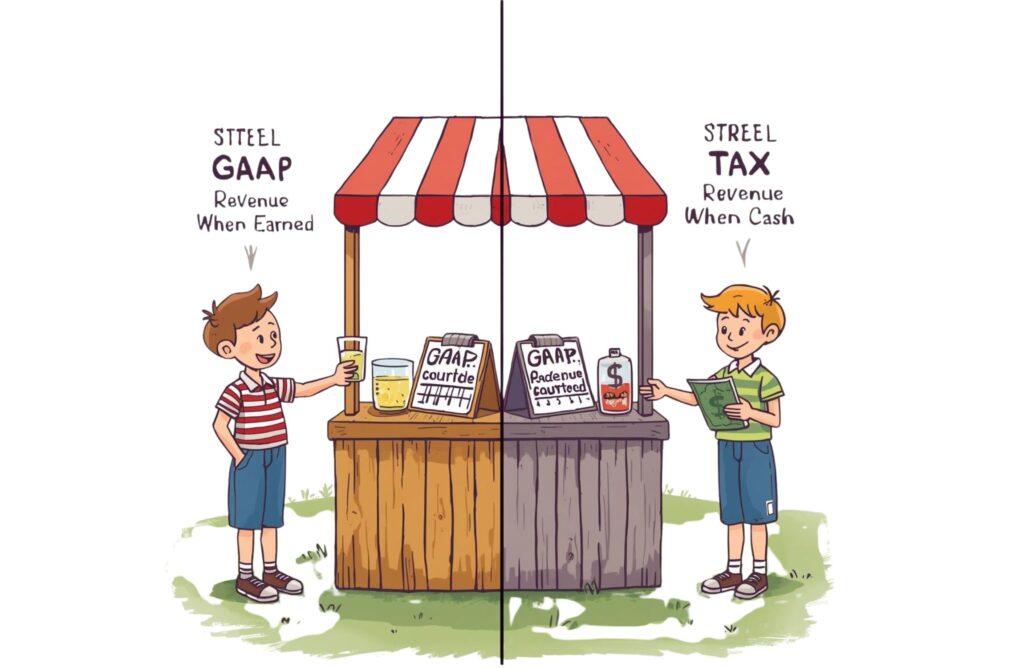

Rule #1: When Do You Count Sales Money? (Revenue Recognition)

Imagine a kid who owns a lemonade stand.

- GAAP’s Rule (Earning the Money): GAAP says you count the money you made as soon as you hand the customer the glass of lemonade. It doesn’t matter if they pay you right now or if they say, “I’ll pay you tomorrow.”

- The Big Idea: This gives a smoother, more predictable idea of how well the lemonade stand is really doing over time.

- Tax’s Rule (Getting the Cash): Tax rules often let the lemonade stand count the money only when the customer actually gives you the cash in your hand.

- The Big Idea: This means the tax report can look “lumpier”—one day the sales number is zero, and the next day, when all the friends finally pay up, the number jumps way up!

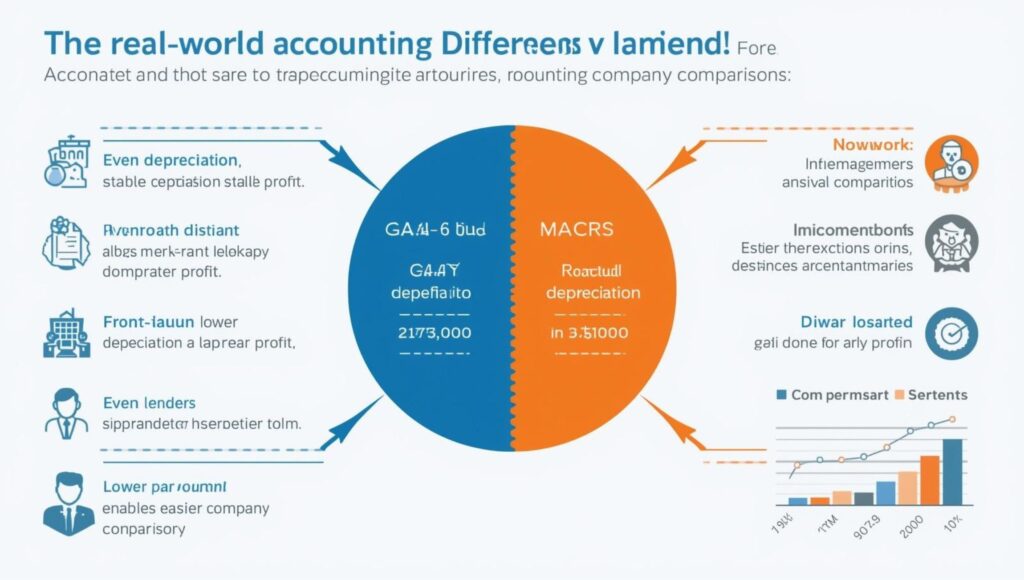

Rule #2: How Do You Count the Cost of Big Stuff? (Depreciation)

When a business buys a big, expensive thing that lasts a long time, like a new ice cream machine, they don’t count the whole cost in one day. They spread the cost out—that’s called depreciation.

- GAAP’s Rule (Straight and Fair): GAAP wants to spread the cost evenly across the machine’s life. If the machine lasts five years, they divide the cost by five and count that much cost each year.

- The Big Idea: This shows the true, slow cost of using the machine to make ice cream each year.

- Tax’s Rule (Fast and Helpful): Tax rules use a special system called MACRS. This system lets the business pretend the cost is much bigger in the first few years (they count the cost much faster).

- The Big Idea: This is a nice incentive from the government! By counting a bigger cost early on, the business’s taxable profit goes down, so they pay less tax right now. But it doesn’t show the machine’s actual wear and tear.

Rule #3: How Do You Track Long-Term Rentals? (Lease Accounting)

Imagine a business rents a big office space or a big delivery truck for many years. That long-term rental is called a lease.

- GAAP’s Rule (The Big List Change): The GAAP rulebook says that if a business rents something for more than one year, they must act like they have a kind of pretend-ownership. They have to put two things on their big money list (the Balance Sheet):

- A “Right-to-Use” Asset (This says they have the right to use the truck/office).

- A Lease Debt (This is the total rent money they still owe for the rest of the years).

- The Big Idea: This makes the GAAP money list more honest about all the business’s long-term promises (debts) so banks can see the true picture.

- Tax’s Rule (Just a Simple Bill): For tax rules, the rental payment is simpler. The business just writes down the rent payment as a regular, simple operating expense (like paying for electricity or gas) only when they pay it.

- The Big Idea: Because the tax report doesn’t show the big, long-term rent debt, the money list for tax purposes will show less debt than the GAAP money list.

Rule #4: Counting Possible Losses (Anticipating Trouble)

- GAAP’s Rule (Being Careful – Prudence): GAAP tells businesses to be careful and anticipate problems. It’s like putting on a helmet before you fall off your bike!

- Bad Bills: If a customer might not pay their bill, GAAP tells the business to immediately set aside a little money in an “Allowance for Doubtful Accounts” to prepare for that loss. This makes the current profit look a little lower, just in case.

- Old Inventory: If the business has toys that are old and nobody wants (obsolete inventory), GAAP requires them to mark the value down right away.

- Tax’s Rule (Waiting for Proof – Realized Losses): The tax law is much stricter. The government says you can only count a debt as a loss when you have proof that the customer will definitely not pay you back. You can’t just guess!

- Similarly, you can’t deduct the cost of old toys until you actually sell them for a cheap price or throw them away.

- The Big Idea: GAAP counts possible losses right away to be safe; Tax waits until the loss is 100% real before allowing a deduction.

Rule #5: Buying Another Company (Goodwill)

When one company buys another, they often pay extra for the company’s good reputation, loyal customers, or special secret recipe. This extra price is called Goodwill.

- GAAP’s Rule (Checking the Value): GAAP says the company must check the value of the Goodwill every year. If the good reputation has gone down (we call this impairment), the company has to write off a big, sudden loss on its money report.

- The Big Idea: This gives an honest, but sometimes bumpy, picture of the company’s true value.

- Tax’s Rule (Steady Deduction): The tax rule is simpler. The government lets the company slowly deduct (or amortize) the cost of the Goodwill evenly over 15 years, no matter what happens to the reputation.

- The Big Idea: The tax report shows a steady, predictable deduction every year, which helps lower taxes a little bit each time.

Other Small Differences

Starting a Business (Start-up Costs):

- GAAP: Says you must count all the beginning costs (like buying office supplies or paying a consultant) as an expense right away when you pay them.

- Tax: The tax rule lets you count up to $5,000 of these costs right away in the first year. You must spread the rest of the costs out and deduct them slowly over the next 15 years.

Fines and Penalties:

- Taking Out a Loan (Getting Borrowed Money):

- When a business takes out a loan, the cash goes up, but the debt (liability) also goes up on both the GAAP and Tax money lists.

- The money you borrow is not counted as taxable income, because you have to pay it back

The Real-World Impact on Stakeholders & Decisions

These accounting differences are not just theoretical; they have tangible consequences for how a business is managed, funded, and perceived by the outside world.

Impact on Financial Performance (EBITDA and Profit)

The way a company does its accounting can change how its profit looks.

1. Different Depreciation = Different Profit

- GAAP spreads asset cost evenly over many years.

- Tax rules (MACRS) let companies show more expense at the start.

2. Profit Numbers Change

Because MACRS shows more early expense:

- Profit looks smaller in the first years.

- EBITDA stays the same, because EBITDA doesn’t count depreciation.

3. Hard to Compare Companies

If two companies use different accounting methods,

their profit will look different, even if the business is the same.

Why Lenders and Investors Like GAAP More

Lenders (bank) and investors want to compare companies easily.

GAAP helps because everyone uses the same rules.

Why GAAP Is Better

- GAAP shows all debts, even lease debts.

- This helps banks see the real financial condition.

- Banks are giving fewer loans now (44% in 2023 → 39% in 2024).

- So clear GAAP reports make a business look strong and trustworthy.

Why Tax Reports Are Not Enough

- Tax reports try to reduce tax, not show full strength.

- This can make a good business look weaker.

- Then investors or banks may not trust the numbers.

Business Owners: Using Both GAAP and Tax Rules

Business owners must understand both systems.

Example: Buying New Machines

- Tax rules (MACRS):

Show big depreciation early → tax bill becomes smaller → more cash saved now. - GAAP:

Shows small depreciation → profit looks higher → good for banks and buyers.

Why This Matters

A business owner must understand both sides:

- Tax side → helps save cash now

- GAAP side → helps show profit and get loans

Both are important for smart planning and growth.

Navigating the Divide: Choosing, Managing, and Reconciling Financial Statements

Given the significant impact, businesses must be deliberate about how they approach financial reporting. The right choice depends on the company’s size, industry, and strategic goals.

Who Uses What: Choosing the Right Reporting for Your Business

For small businesses with no loans and no outside investors, tax-basis financial statements are enough. They are cheaper and help with tax filing. But if the business grows, needs a loan, or plans to sell, GAAP statements become important. Many small businesses are growing. A Bank of America survey found that 55% of small businesses had higher revenue in 2023. These businesses will face more pressure from banks and investors to use GAAP, because GAAP shows a clear picture of the company’s finances.

Bridging GAAP and Tax Reports (Differences)

Most businesses keep one set of books. Usually, it is tax-based, because it is simple and cheap. When they need GAAP reports, they make small changes to match GAAP rules.

How It Works

- They check differences between tax rules and GAAP rules.

- Common changes (called Schedule M-1 or M-3) are:

- Depreciation – how the cost of things like machines is spread over years

- Revenue timing – when money earned is counted

- Non-deductible expenses – costs that tax does not allow

These changes connect tax income and GAAP income, so both numbers make sense.

Accounting Tools and Tips

Modern software can help your team do both GAAP and tax reports.

It can track different depreciation and tag transactions easily.

Best Practices

- Keep simple records for:

- Machines and equipment

- Leases

- Allowances (like bad debts)

- This helps to:

- Make accurate reports for GAAP and tax

- Easier reconciliation at year-end

Tip: Good records = less mistakes, easier accounting

Conclusion: Easy Financial Reporting

Choosing between GAAP and tax reports is not just about numbers.

It is a smart choice that shows how banks, investors, and partners see your business.

- Tax reports → good for tax filing.

- GAAP reports → show a clear and trusted picture for growth and loans.

Key Idea

- Tax basis asks: “How much tax do I pay?”

- GAAP asks: “What is the true picture of my company?”

- Knowing this helps you use both correctly.

Why It Helps Your Business

- As your business grows, you need better reports.

- Using the right system helps you get loans, attract investors, and plan well.

- Financial reporting is a tool to grow your business, not just a rule.

Final Tip

Use good accountants. They help you follow tax rules and make clear GAAP reports. This builds trust with banks and investors and helps you make smart decisions.

Learn More About LLC Termination in Texas, IRS Tax Kiosk Closures