Small businesses don’t pay a single flat tax rate — how much they’ll owe in taxes depends largely on factors such as their business structure, income and location. The average small business in the United States pays more than 19.8% of its income toward taxes, the firm added, though this distribution varied significantly by entity type:

Sole proprietorships: Are taxed at the owner’s individual income tax rate, which has averaged around 13.3% of gross receipts. A tax return must be filed for net earnings from self-employment of $400 or more.

Partnerships: They also employ a pass-through structure, whereby people are taxed on their share of the entity’s net income. Small partnerships have an average rate of around 23.6%.

S Corporations (S Corps): Just like partnerships, profits flow through to owners’ individual returns. The mean rate is about 26.9 percent.

C Corporations (Regular corporations): Are the only type of entity that are taxed federally as if they were its own person and have to pay a federal corporate tax rate of 21% on all net profits.

This definitive guide is designed to demystify that complexity. By following along, you will learn the precise factors that determine your tax liability, from your foundational business structure to the specific federal, state, and local taxes you’ll encounter. We will move beyond abstract rates to explore the tangible costs you must budget for. To get the most out of this guide, have a basic understanding of your business’s revenue and major expenses. By the end, you’ll be equipped to understand your tax obligations, anticipate your costs, and make informed financial decisions for your business.

How Much Do Small Businesses Pay in Taxes?

Most small businesses (like over 90%) are pass-through entities (sole proprietorships, partnerships, LLCs, or S corps). That means the business profits go straight to your personal tax return, and you pay federal income tax at individual rates, which range from 10% to 37% depending on your total income.

Many owners also get a 20% qualified business income (QBI) deduction, which can lower the effective rate on business profits quite a bit—often bringing it down to around 15-30% federal after that.

On top of that, if you’re self-employed (like a sole prop or single-member LLC), you pay self-employment tax of 15.3% on net earnings (that’s for Social Security and Medicare—you can deduct half of it on your income tax).

Studies show the average effective federal tax rate for small businesses is around 19-20% overall. It breaks down like this by type:

- Sole proprietorships: often lower, around 13-20%

- Partnerships: about 23-24%

- S corps: closer to 26-27%

If your business is a C corporation (less common for small ones), it pays a flat 21% federal corporate tax on profits. Then, if you take money out as dividends, you pay personal tax on that too (double taxation).

Don’t forget state taxes—most states add 0-11.5% on top (some have none), plus possible local taxes, sales tax if you sell stuff, payroll taxes if you have employees (about 7.65% employer share for FICA), and property taxes.

The real amount you pay comes down to your net profit after expenses and deductions. Lots of small business owners end up paying 20-30% total when including federal, state, and self-employment taxes, but smart deductions (home office, mileage, equipment, health insurance) can drop that a lot.

What Small Business Owners Need to Know About Taxes

For small business owners, taxes are not a once-a-year event but an ongoing financial reality. The amount you pay is a direct result of several key variables. The most critical is your business structure, which dictates how your income is taxed—either at the corporate level or on your personal return. Next are your federal obligations, which include income tax, self-employment taxes for Social Security and Medicare, and payroll taxes if you have employees. Finally, your geographic location adds another layer, with each state and municipality imposing its own set of income, sales, property, and other specific taxes. Understanding these interconnected elements is the first step toward gaining control over your financial planning.

The “Costs” Beyond the Rates: Understanding Your Full Tax Burden

Your true tax cost extends far beyond a simple income tax percentage. It’s a comprehensive figure that includes multiple layers of financial responsibility. You must account for federal and state income taxes, the 15.3% self-employment tax for unincorporated businesses, and employer-side payroll taxes if you have a team. Furthermore, there are often annual fees for maintaining your legal entity, renewing a necessary business license, or paying a state franchise tax simply for the privilege of operating. These ancillary costs, while smaller individually, accumulate and form a significant part of your total financial obligation to government entities. Budgeting effectively requires looking at this complete picture, not just the headline income tax rate.

The Foundation: How Your Business Structure Dictates Tax Liabilities

The single most important decision impacting your Small Business Taxes is your choice of business structure. This legal framework doesn’t just define your liability protection; it fundamentally determines the tax forms you file, the rates you pay, and whether the business itself or you as the owner pays the income tax.

Sole Proprietorships & Independent Contractors (Self-Employed Individuals)

This is the simplest business structure, with no legal distinction between the owner and the business. As a sole proprietor, you report all business income tax on your personal tax return using Schedule C (Form 1040). The profits are taxed at your individual income tax rates. This structure is considered one of the primary pass-through entities (or pass-throughs), as the profits “pass through” to the owner’s personal return. You are also responsible for paying self-employment taxes (Social Security and Medicare) on all your net earnings.

Partnerships

A Partnership is a business owned by two or more individuals. Like a sole proprietorship, it is a pass-through entity. The partnership itself does not pay income tax. Instead, it files an informational return, Form 1065, with the Internal Revenue Service (IRS) detailing its income, deductions, and credits. This information is then passed to the partners via a Schedule K-1. Each partner reports their share of the profits and losses on their personal tax return and pays income tax at their individual rate, along with self-employment taxes on their portion of the earnings.

Limited Liability Companies (LLCs)

Limited Liability Companies (LLCs) offer a unique blend of liability protection and tax flexibility. By default, the IRS treats an LLC based on its number of owners. A single-member LLC is taxed like a sole proprietorship (a “disregarded entity”), and a multi-member LLC is taxed like a partnership. However, an LLC can formally elect to be taxed differently. It can choose to be treated as an S corporation or even a C corporation, allowing owners to select the tax structure that best suits their financial goals without changing their legal structure.

S Corporations (S Corp)

An S corporation (S Corp) is a tax election available to LLCs and corporations, allowing them to function as pass-through entities where profits and losses are reported on shareholders’ personal tax returns via Schedule K-1. Unlike sole proprietorships or partnerships, S Corp owners who work in the business must receive a reasonable salary subject to payroll taxes, while remaining profits can be distributed as dividends, which are not subject to self-employment taxes, leading to potential tax savings.

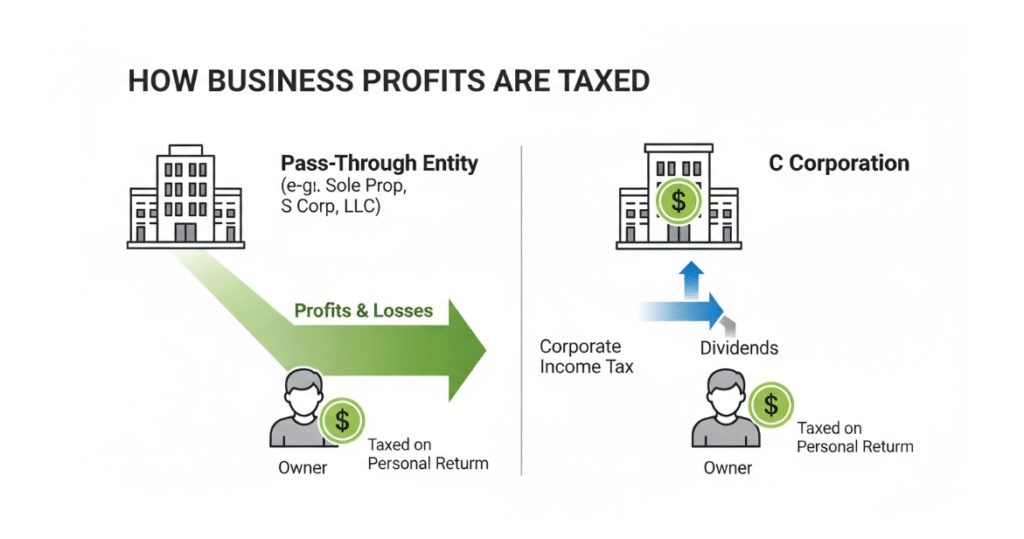

C Corporations (C Corp)

A C corporation is a distinct legal and tax entity, completely separate from its owners. Unlike pass-throughs, the corporation itself pays federal income tax on its profits at a flat 21% rate. It reports this income on Form 1120. If the corporation then distributes profits to shareholders as dividends, those shareholders must pay personal income tax on that dividend income. This creates a potential for “double taxation”—once at the corporate level and again at the individual level. While this structure is more complex, it offers benefits for reinvesting profits back into the business and providing extensive fringe benefits to owners.

Federal Tax Obligations: The Core of Your Small Business Tax Bill

The Internal Revenue Service (IRS) administers federal taxes, which typically form the largest portion of a small business’s tax liability. These obligations are consistent nationwide, though how they apply depends directly on your business structure and whether you have employees.

Federal Income Tax

This is the primary tax on business profits. For C corporations, the calculation is straightforward: a flat 21% federal corporate income tax on taxable profits. For all pass-through entities—sole proprietorships, partnerships, LLCs taxed as such, and S Corps—the process is different. The business’s net income “passes through” to the personal tax returns of the owners. These small business owners then pay income tax on that profit based on their individual marginal tax brackets, which currently range from 10% to 37%.

Self-Employment Tax

This tax is a critical component for owners of pass-through businesses. It is the self-employed individual’s version of the Social Security and Medicare taxes (FICA) that employees and employers split. The self-employment tax rate is 15.3% on the first $168,600 of net earnings (for 2024) and 2.9% on earnings above that threshold. This tax applies to all net profits for sole proprietors and partners. For S Corp owners, it only applies to their “reasonable salary,” not to profit distributions. C Corp owner-employees do not pay self-employment tax; they pay their share of FICA taxes through payroll deductions.

Federal Employment Taxes (Payroll Taxes)

If your business hires employees, you enter the world of employment taxes. These are separate from your income tax obligations. As an employer, you are responsible for withholding federal income tax, Social Security tax (6.2%), and Medicare tax (1.45%) from your employees’ wages. Crucially, you must also pay an employer’s matching share of Social Security and Medicare taxes. Additionally, you must pay Federal Unemployment Tax (FUTA), which is 6% on the first $7,000 of each employee’s wages, though credits for state unemployment tax payments can significantly reduce this rate.

State and Local Taxes: A Complex Layer

Once you’ve addressed your federal obligations, you must navigate the intricate and highly variable landscape of state and local taxes. Your tax burden can change dramatically depending on which state your business operates in. This geographic factor is as important as your business structure in determining your total tax cost.

State Income Tax

Most states impose an income tax on businesses. Similar to the federal system, the application varies by business structure. C corporations typically pay a corporate income tax directly to the state, with rates ranging from zero in some states to nearly 10% in others. For pass-through entities, the business income flows to the owners’ personal returns, who then pay personal income tax to the state based on their individual brackets. Several states, such as Texas, Florida, and Washington, have no personal or corporate income tax, offering a significant tax advantage.

State Sales Tax

If your business sells taxable goods or services, you are generally required to collect sales tax from customers and remit it to the state. Sales tax rates vary widely by state and even by locality (city or county). While this tax is collected from the customer, the administrative burden of tracking, collecting, and remitting these funds falls squarely on the small business owner. Failure to comply can result in significant penalties.

Gross Receipts Tax

A handful of states, including Ohio, Washington, and Delaware, impose a Gross Receipts Tax (GRT) either instead of or in addition to a corporate income tax. Unlike income tax, which is levied on profits (revenue minus expenses), a GRT is calculated based on the business’s total revenue. This means a business could owe GRT even if it didn’t make a profit for the year, making it a particularly challenging tax for low-margin businesses.

Property Tax

If your business owns real estate, such as an office, warehouse, or retail space, you will be subject to local property taxes. These taxes are assessed by municipal or county governments based on the value of the property and are a significant ongoing expense. Some jurisdictions also levy property taxes on business personal property, such as machinery, equipment, and inventory.

Other State and Local Taxes and Fees

Beyond the major taxes, businesses often face a variety of other state and local levies. A common example is the franchise tax, which is a fee paid to the state for the privilege of doing business there. It is often based on a business’s net worth or capital, not its income. Additionally, nearly every business must obtain and annually renew a business license or permit from its city or county, which comes with a fee that contributes to the overall cost of compliance.

Managing Your Tax Burden: Deductions, Credits, and Planning

Understanding your tax rates is only half the battle; actively managing your tax liability is how you can directly impact your bottom line. Through strategic use of deductions, credits, and meticulous record-keeping, you can legally reduce the amount of income subject to taxation.

Common Business Tax Deductions

Deductions are expenses that the IRS deems “ordinary and necessary” for conducting your business. By subtracting these from your gross income, you lower your taxable income and, therefore, your tax bill. Common deductions for a business include:

- Startup Costs: Up to $5,000 in the first year.

- Vehicle Expenses: Using either the standard mileage rate or actual expenses.

- Salaries and Wages: Compensation paid to employees (and reasonable salaries for S Corp owners).

- Office Supplies and Rent: Costs for your workspace and materials.

- Insurance: Premiums for business liability, health insurance (for employees), and other policies.

- Professional Fees: Payments to lawyers, accountants, and consultants.

- Qualified Business Income (QBI) Deduction: A significant deduction for many pass-through entities, allowing them to deduct up to 20% of their qualified business income.

Key Tax Credits for Small Businesses

While deductions reduce your taxable income, tax credits reduce your actual tax bill on a dollar-for-dollar basis, making them even more valuable. Key credits available to small businesses include:

- Small Business Health Care Tax Credit: For employers who contribute to their employees’ health insurance premiums.

- Work Opportunity Tax Credit (WOTC): For hiring individuals from certain targeted groups facing barriers to employment.

- Credit for Small Employer Pension Plan Startup Costs: Helps offset the costs of starting a retirement plan like a 401(k) or SEP IRA.

The Importance of Accurate Bookkeeping and Record-Keeping

Effective tax management is impossible without pristine financial records. Accurate bookkeeping provides the data needed to claim every eligible deduction and credit. It creates a clear audit trail to substantiate your tax filings if the IRS ever has questions. Meticulous records of income, expenses, receipts, and payroll are not just a compliance requirement; they are a fundamental tool for making strategic financial decisions and minimizing your tax burden.

The Reality of “Costs”: Budgeting for Small Business Taxes

Successfully managing small business finances requires translating abstract tax rates into a concrete financial plan. This means budgeting not just for a year-end tax bill but for a series of ongoing costs and payments that are integral to staying compliant and financially healthy.

Translating Rates into Actual Financial Impact

An effective tax rate of 25% doesn’t mean you simply set aside one-quarter of every dollar that comes in. You must first calculate your net income by subtracting all deductible expenses from your revenue. The tax is paid on this profit. For example, a business with $100,000 in revenue and $60,000 in expenses has a net income of $40,000. A 25% tax would be applied to that $40,000, resulting in a $10,000 tax bill, which is only 10% of the total revenue. Understanding this distinction is vital for accurate cash flow planning.

Quarterly Estimated Taxes: Paying as You Go

The U.S. tax system is “pay-as-you-go.” For most small business owners (everyone except C Corp employees who have taxes withheld), this means you can’t wait until April to pay your entire tax bill for the previous year. You are required to estimate your annual tax liability (including income and self-employment taxes) and pay it to the IRS in four quarterly installments. Failure to pay enough tax throughout the year can result in underpayment penalties.

Annual Regulatory Compliance and Renewal Costs

Your total tax-related outflow includes more than just payments to the IRS and state tax authorities. You must also budget for annual compliance costs. This includes fees for renewing your business license or permits, paying your state’s annual report filing fee to keep your LLC or corporation in good standing, and potentially paying a state franchise tax. These costs are a predictable part of doing business and should be included in your annual budget.

Common Small Business Tax Mistakes and How to Avoid Them

Even the most diligent small business owners can make costly tax errors. Being aware of common pitfalls is the first step in avoiding them and ensuring your business remains compliant and financially sound.

Misunderstanding Your Business Structure’s Tax Implications

One of the most frequent and significant errors is choosing a business structure without fully grasping its tax consequences. For example, an owner of a profitable LLC taxed as a sole proprietorship might be paying thousands more in self-employment taxes than if they had elected S Corp status and paid themselves a reasonable salary. Conversely, forming a C corporation without a clear strategy for reinvesting profits can lead to unexpected double taxation. It is crucial to review your structure with a professional as your business grows and its financial situation evolves.

What’s Next?

This guide has decoded the complex question of how much small businesses pay in taxes, revealing that the answer lies in a combination of your business structure, federal obligations, and state-specific levies. We’ve established that there is no single tax rate; instead, your liability is a unique calculation based on your entity type—from pass-throughs like sole proprietorships and partnerships to separate entities like C corporations. You now understand that your true cost includes not just income tax but also self-employment taxes, payroll taxes, and state-level fees like franchise taxes and business license renewals.

Armed with this knowledge, your next steps are clear and actionable:

- Confirm Your Tax Treatment: First, definitively identify how your current business structure is treated for tax purposes. If you run an LLC, are you being taxed as the default (sole proprietorship/partnership) or have you made an S Corp or C Corp election? This is the bedrock of your tax plan.

- Implement Robust Bookkeeping: If you haven’t already, establish a meticulous system for tracking all income and expenses. This is non-negotiable for maximizing deductions and ensuring you can defend your tax position. Use accounting software or hire a bookkeeper.

- Estimate and Plan for Quarterly Payments: Use your records to project your net income for the year. Calculate your estimated income and self-employment tax liability and divide it by four. Set calendar reminders for the quarterly deadlines (typically April 15, June 15, September 15, and January 15) to avoid penalties.

- Consult a Tax Professional: The complexities of tax law, especially with strategies like the S Corp election or navigating multi-state operations, warrant expert advice. Schedule a consultation with a qualified accountant or CPA to review your specific situation and create a proactive tax strategy.

By treating tax planning as an integral, year-round business function rather than an annual chore, you can move from a reactive position to one of control, ensuring compliance and optimizing your financial health for the long term.

Recommended Post: